Why Spring is a Prime Time for Real Estate Spring consistently ranks as one of…

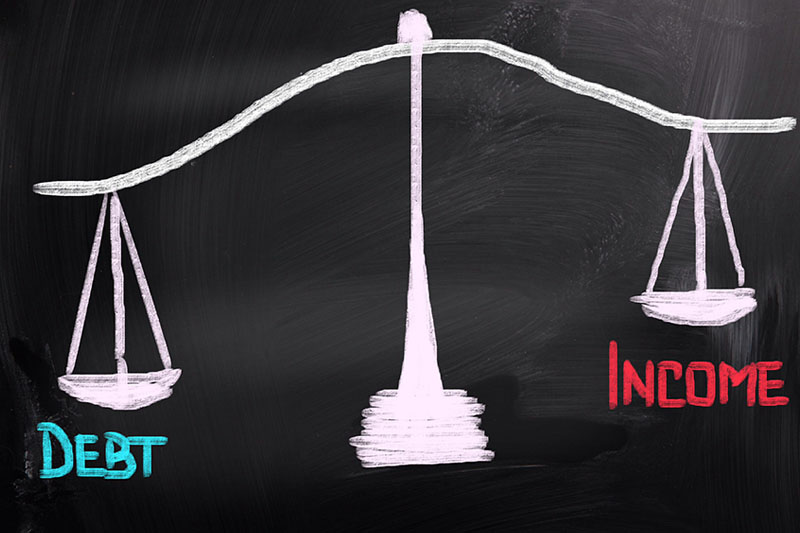

Understanding Debt-to-Income Ratio When Buying a Home

Most homebuyers get a loan to purchase their property called a mortgage. This is a specific type of loan that banks and credit unions offer to make home ownership possible without saving up hundreds of thousands of dollars to purchase it outright. But potential mortgage candidates must still take certain financial steps to get approved for this loan. One of the most important factors that lenders consider is the applicant’s debt-to-income ratio, DTI.

What is DTI?

Your DTI is the ratio of your existing debts to your existing income each month. Your lender will ask you to disclose all debts, such as student loans, car loans, credit cards, and others. They will then add up the monthly payments to get your total monthly debt expense. They will do the same for your income, including any W-2 income and 1099 income as it is noted on your taxes. They will verify this information using your tax returns and credit report.

What is my DTI if I’m married?

If you are applying for a mortgage with your spouse, your lender will include all debts and all income that you both have listed. This includes individual debt and income as well as shared debts. If you are applying for a mortgage with just one spouse listed on the loan, they will only include the debt and income under that spouse’s name. Keep in mind that you may still be listed as responsible for a spouse’s debt, even if your spouse is not included on the mortgage application. It is best to disclose any and all debt that could be included in your monthly expenses.

How to I improve my DTI?

To lower your DTI, you can lower your debt or increase your income. Most lenders look for a DTI of 50% or less, although this can vary by lender and by type of mortgage. One of the fastest ways to reduce your DTI is to pay off debts that have a high monthly payment. These are often personal loans, credit cards, and car loans. You can also work to increase your income, although this can often take longer to impact your DTI.